How long will it take to reach financial independence

Reaching financial independence takes time and discipline. How long will it take you to get there?

In this post we explain how to calculate your FI timeline along with a few short comings of this approach.

Table of contents

Introduction

If you've been interested in financial independence for more than 15 minutes, you're likely to have come across the 4% rule. In a nutshell, this rules states that once you've accumulated savings to the value of 25 times your annual expenses, you've reached financial independence. At that point, you can then live off the capital by withdrawing 4% from it annually and are very unlikely to run out of money.

There's more to the 4% rule than the above summary, but that's good enough for the purposes of this post.

One of the first questions that often come up around financial independence is, how long will it take me to get there?

Calculating your timeline to financial independence

Unfortunately most people use a fairly simplistic approach to calculating how long it will take to reach financial independence. There's nothing wrong with this for a rough guide, but it's not representative of the real world and leaves some rather large elephants walking round the room.

Never the less, I'll illustrate this approach now and then circle back to the short comings of it further down. Feel free to skip ahead past the math.

Step 1: Calculate your current FI number

Take your current annual expenses and multiply this by 25.

eg: $40 000 * 25 = $1 000 000

Step 2: Future value of annuities

The above FI number is essentially the result of a future value of annuities calculation. Here's the formula for those that are interested:

FI number = (Savings rate) * [(1 + compounding rate)^^Time – 1] / (compounding rate)

Step 3: Rearrange the formula to solve for time

Notice that one part of the above formula is time. Therefore we can rearrange the formula to determine time, ie: how long will it take us to reach FI.

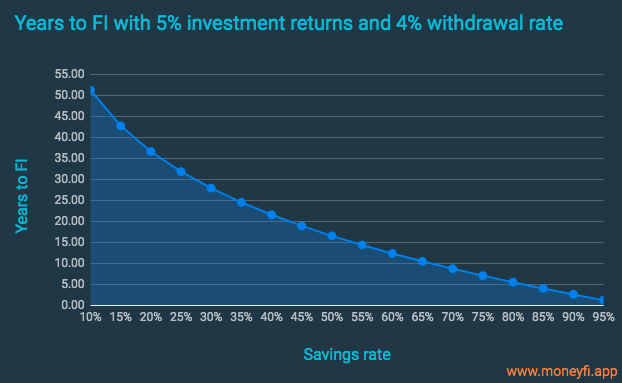

In the below chart, I've run this calculation across multiple different savings rates to determine years to FI using the 4% rule and a 5% investment return:

So far so good. Charts like these are fairly common in the FI community. As you increase your savings rate, years to FI decreases. This is a great place to start and gives us a rough guide to how long it might take to reach FI.

Now lets get back to those elephants walking around the room.

Our finances aren't set in stone

If we really want to understand how long it will take to reach financial independence then we need to incorporate our ever changing finances into the calculations.

Perhaps you're considering purchasing a home in a couple years from now. The above calculation doesn't take into account mortgage payments, insurance and repairs that don't currently exist in your expenses.

Perhaps you're considering having a child (or another child) in a few years from now. Once again, the above calculation doesn't take into account school fees, medical costs, clothing etc that don't currently exist in your expenses.

Perhaps you're considering dropping down to part time work in a few years from now so that you can focus on other interests. How do you account for that in the above calculations? Unfortunately, you can't.

That's just 3 examples, but hopefully they're enough to illustrate that our finances aren't set in stone. Simply multiplying our current annual expenses by 25 and then using that to figure out our timeline to FI isn't good enough. In fact for most of us, that number is complete fiction.

Including future life events in your FI timeline

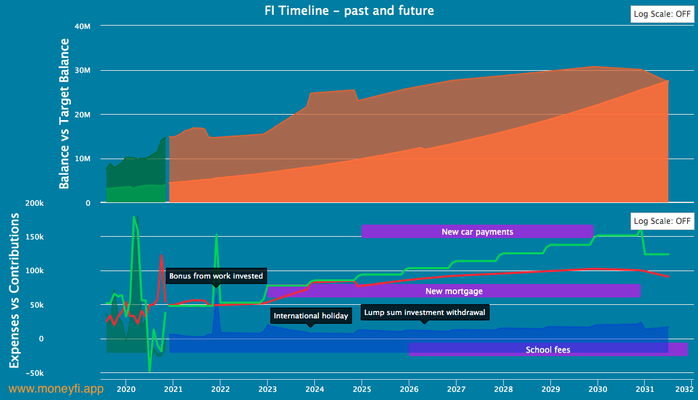

The above chart and the calculations used to create it are enough for a rough, pie in the sky timeline for reaching FI. However Money FI provides the ability to model future life events, inflation and changes to your finances to create an accurate projection of your journey to financial independence.

The below chart was created using Money FI and includes a few once off and recurring life events to illustrate a real timeline to financial independence. The green sections on the left are historical and therefore track your actual progress to FI. To the right is the forward looking projection.

Having a way to incorporate our ever changing interests, obligations, finances and future life events into our FI timeline is at the core of why Money FI exists.

Money FI allows you to create comparisons along your timeline to quickly see what the impact of possible future financial decisions will be. This is a great way to determine if buying that flashy new car is really worth it in the long run after seeing the impact it will have on your timeline.

Conversely, creating comparisons along your timeline can highlight ways to enjoy the journey just as much as the destination. It's often surprising to find that things which you thought would have a big impact on your timeline actually don't, and you should therefore stop stressing about them.

Article by Brendon @ Money FI